Economic System

Introduction: A Pattern for Productive Stewardship and Sustainable Prosperity

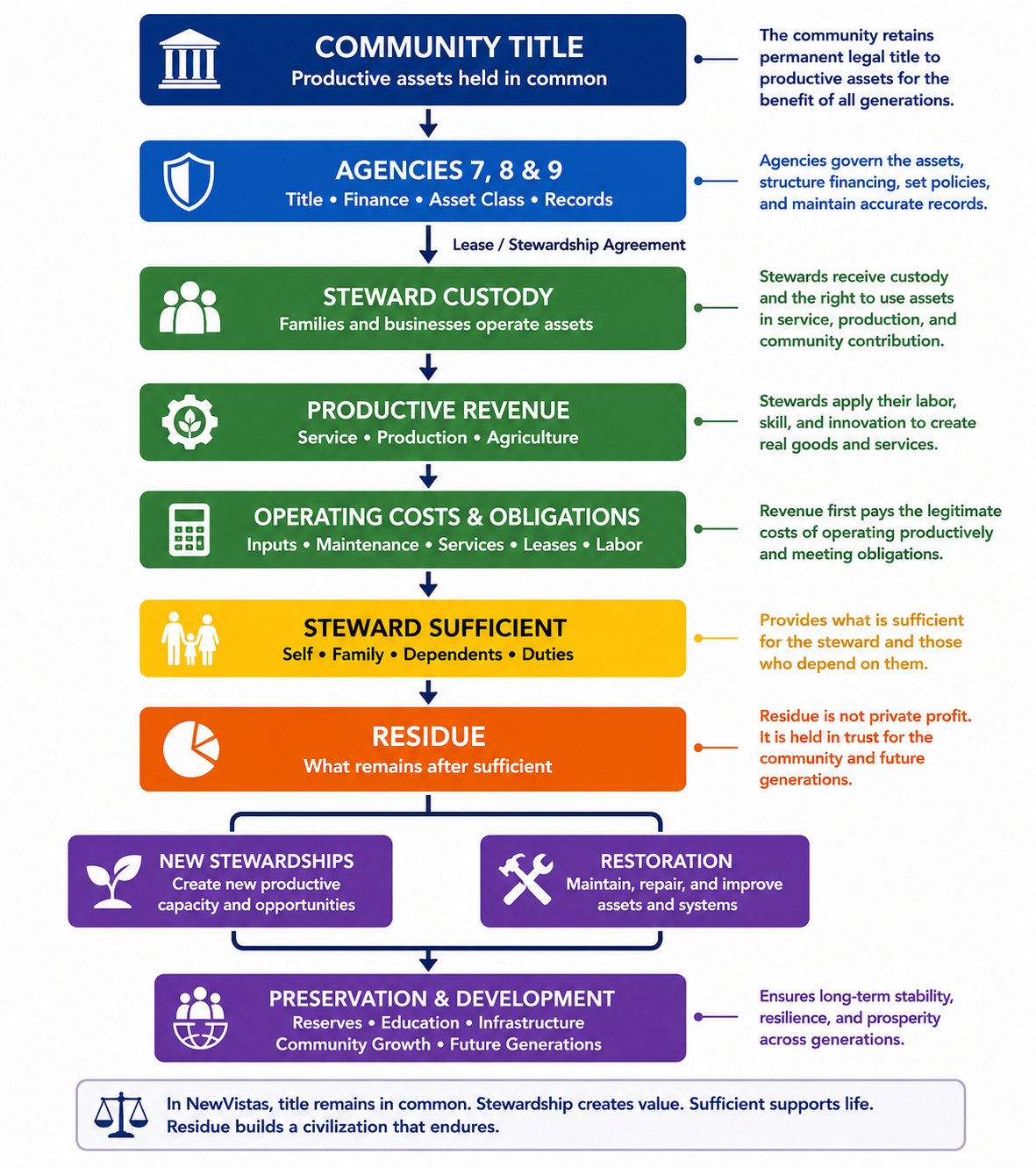

A NewVistas economic community is designed to make land, housing, equipment, work, credit, accounting, and essential services operate as one carefully governed system. Its purpose is to enable the community to live up to its core principles of “no poor among them,” and “all things in common.”

After separating different kinds of capital into different governing channels, the system assists stewards to access these items through well-coordinated and structured processes. Each type of asset, whether short-term assets, long-term assets, or equipment, is governed by a particular agency, which has an autonomous bank relationship, and its own method of resolving failure. This separation is one of the main safeguards of the NewVistas economic model.

Infrastructure preservation is treated as a constitutional duty. Productive infrastructure must never be consumed faster than it can be maintained, repaired, and replaced. Housing, equipment, utilities, transportation systems, communications systems, and productive tools are therefore governed according to long-term stewardship rules intended to preserve continuity across generations.

Stewardship Instead of Debt Dependency

NewVistas does not eliminate personal enterprise. In many ways, it seeks to strengthen it.

The system restructures the relationship between individuals and capital so that people can remain productive without becoming trapped in unstable debt structures or speculative ownership cycles. Participants retain operational freedom, productive initiative, and the ability to build useful enterprises, while the underlying infrastructure and title systems are constitutionally governed to preserve long-term stability.

Participants work through stewardship plans, which are structured plans for producing goods, services, care, maintenance, education, food, transport, technology, and other useful work.

A steward may use housing, land, equipment, devices, tools, vehicles, furniture, fixtures, or workspaces, but these assets are governed through the community’s title and financing system. The steward receives use rights and operating authority under verified plans rather than personally borrowing to purchase everything outright.

This allows productive life to continue without forcing every participant into large personal debt obligations merely to gain access to the tools of economic participation.

A Market Economy With Constitutional Safeguards

NewVistas remains a market-based economy in which supply and demand continue to influence prices, production, and economic coordination. The system does not attempt to abolish markets or replace all economic decisions with centralized planning.

Instead, it attempts to establish constitutional safeguards around the foundational systems upon which markets depend.

The model is built around two guiding principles. First, no person within the community should fall into destitution or abandonment. Second, productive assets that sustain community life should remain continuously maintainable and accessible across generations.

For this reason, many productive assets are held within structured stewardship systems rather than fragmented into speculative ownership patterns. Land, infrastructure, equipment, and certain productive systems remain governed assets that are accessed through leases, stewardship rights, operational plans, and constitutional financing structures.

The purpose is not to eliminate enterprise, but to prevent the long-term deterioration of the productive foundation upon which enterprise depends.

Agency-Separated Capital Governance

The NewVistas economy is built around the principle that different forms of capital should not be blended together into one undifferentiated financial structure.

Agency 7 governs financial reserves and liquidity. Its role is to maintain settlement integrity, reserve discipline, and financial stability across the broader system. Agency 7 is therefore not treated as a universal bailout authority for every failed operation or financing structure within the community.

Agency 8 governs long-duration property, including land, buildings, infrastructure, and certain long-term property rights. Agency 8 works through its own dedicated property-bank relationship. That bank finances only Agency-8-titled property, takes liens only against Agency-8 property assets, and relies on property lease cashflows for debt service.

Agency 9 governs productive equipment, including machinery, appliances, furniture, vehicles, tools, computing systems, industrial equipment, and heavy plant. Agency 9 maintains a separate equipment-bank relationship dedicated solely to equipment-class assets. The bank takes liens only against Agency-9-titled equipment and finances assets according to their expected service life.

This constitutional separation ensures that failures in one category of capital do not automatically destabilize every other part of the economy.

Financing Based on Real Productive Life

NewVistas financing structures are tied to the actual operational life of assets rather than to arbitrary lending cycles.

A heavy industrial machine may remain productive for decades and may therefore receive long-duration financing. A computing device or networking system may require replacement within only a few years and therefore operates under a much shorter replacement and depreciation cycle.

Agency 9 governs these asset-life schedules in coordination with Agency 16 accounting systems and Agency 18 maintenance and lifecycle rules. Reserve accumulation, maintenance schedules, replacement planning, and depreciation are all tracked continuously so that productive assets do not quietly deteriorate over time.

This structure is intended to preserve the long-term productive capacity of the community rather than allowing infrastructure and equipment to decay through neglected replacement planning.

Credit Through Stewardship Plans

The NewVistas model differs from conventional economies in the way credit is created and distributed.

The system does not depend primarily on unsecured personal borrowing or unrestricted consumer debt structures. Instead, financing authority is tied to steward business plans and verified productive activity.

Before financing proceeds, operational structures are reviewed through Agency 3 governance processes, followed by TOK authorization and financing verification procedures. Property and equipment financing therefore occur only after the relevant agencies confirm that the proposed activity, asset classification, collateral structure, and repayment assumptions meet constitutional requirements.

Participants do not operate through large personal borrowing accounts intended for unrestricted consumption. Instead, spending authority exists through structured business-plan credit allocations connected to productive stewardship activity.

This ties credit to real economic function rather than speculative personal lending.

Failure Resolution Without Systemic Contagion

One of the major goals of the NewVistas economic structure is to prevent failures in one sector from spreading uncontrollably into unrelated parts of the system.

If a steward operation using Agency-9-financed equipment fails, the resolution process focuses primarily on the equipment itself. Assets may be repossessed, reassigned, re-leased, or redeployed into other productive uses. The equipment bank does not gain access to Agency 7 reserves or unrelated property collateral.

Similarly, Agency 8 property financing failures remain within the long-duration property structure governed by Agency 8 and its associated property bank.

This separation allows financial discipline to exist without turning every localized failure into a wider economic collapse.

A Durable Economic Structure

NewVistas does not attempt to create stability merely through subsidies or emergency intervention. Instead, it attempts to build an economic structure in which land, housing, infrastructure, equipment, accounting, and financing are all governed according to long-term stewardship principles.

Participants remain individually responsible for their work and stewardship obligations. At the same time, the surrounding economic structure is designed to preserve productive capital, maintain replacement capacity, reduce destructive debt dependency, and prevent systemic financial contagion.

The goal is not simply economic growth in the short term. The goal is the preservation of productive civilization across generations.

Conclusion

The NewVistas economic system is a stewardship-based economic framework built around constitutional separation of capital classes, disciplined financing, and long-term productive maintenance.

It preserves markets and productive enterprise while protecting the foundational systems upon which economic life depends. Credit is tied to productive stewardship rather than speculative personal borrowing. Asset financing is matched to real service life. Reserve and replacement schedules are continuously maintained. And productive infrastructure is treated as something to be preserved rather than consumed.

The result is an economy designed not merely for immediate efficiency or short-term profit, but for continuity, resilience, productive freedom, and intergenerational durability.