Agency 7: Clearing

Introduction: Agency 7 Constitutional Domain

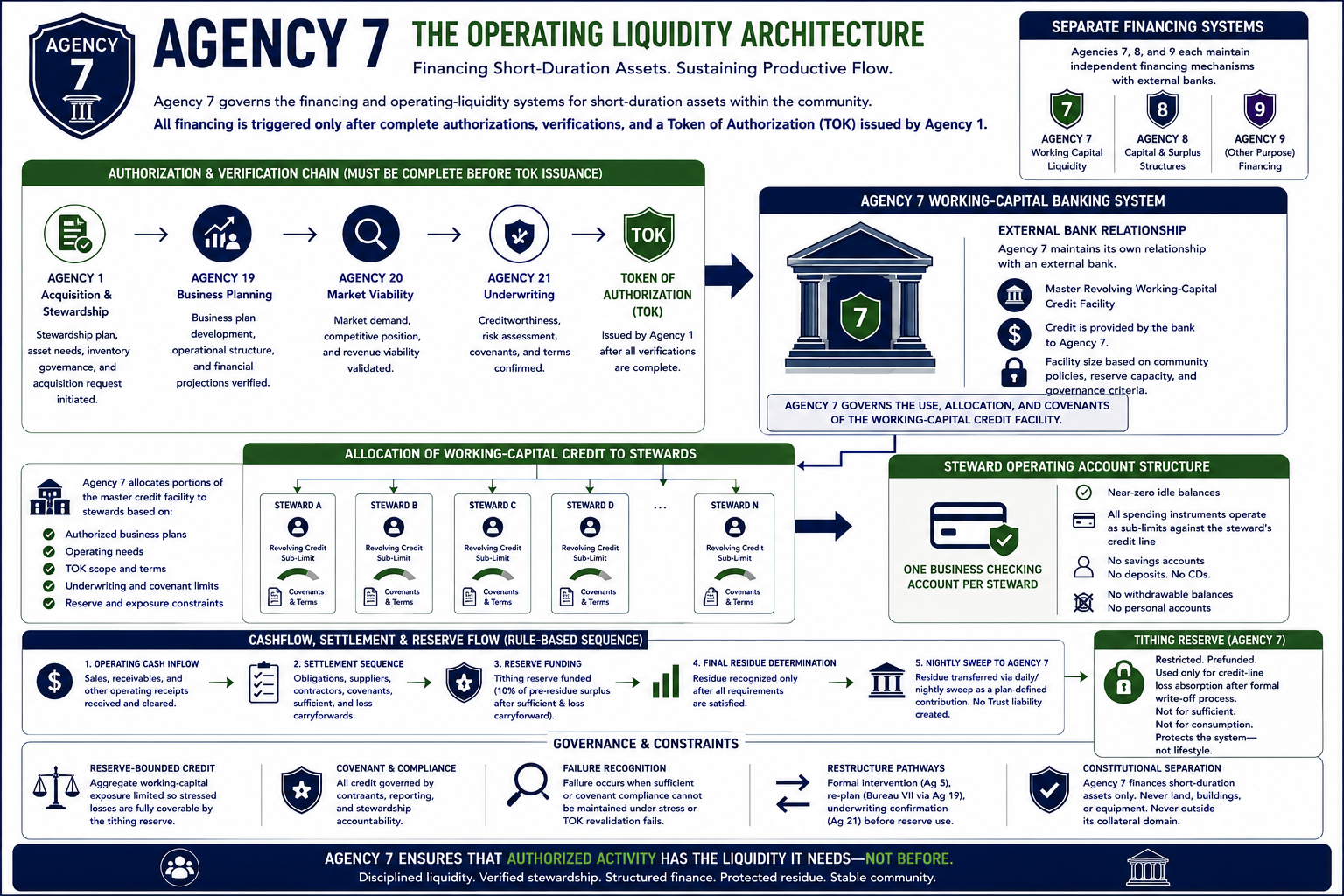

Agency 7 governs the financing and operating-liquidity systems associated with short-duration productive assets within the community. Its constitutional domain includes revolving working-capital financing, inventory collateralization, receivables financing, operating cashflow settlement, covenant governance, short-duration collateral administration, and the liquidity systems that sustain ordinary productive activity throughout the community economy.

The agency exists so that it can facilitate the financing of short-duration assets whose acquisition standards and replenishing mechanisms are governed by agency 1. Every steward, as a business owner, uses the services offered by both agencies as a means of securing inventory that is sufficient and is of merchantable quality. While Agency 1 governs acquisition authorization, stewardship processes, inventory governance, and Token of Authorization issuance, Agency 7 governs the financing systems that activate once those constitutional authorizations are complete.

The constitutional structure intentionally separates acquisition governance from financing governance. Agency 1 governs whether productive acquisition should occur. Agency 7 governs the operating-liquidity systems that allow those authorized activities to function continuously throughout the community.

The issuance of a Token of Authorization therefore functions as one of the principal constitutional triggers for Agency 7 financing activity. Once TOK verification and related lease, underwriting, insurance, and stewardship validations are completed through the appropriate constitutional agencies, certified contractors may execute the corresponding working-capital financing structures governed by Agency 7.

The agency does not finance land, buildings, durable infrastructure, or permanent equipment. Those systems remain constitutionally separated under the appropriate agencies governing long-duration capital assets. Agency 7 governs only short-duration operating assets and the revolving liquidity structures necessary to sustain productive continuity.

The agency exists because communities become unstable when operating liquidity becomes detached from productive stewardship. Modern financial systems frequently merge consumer banking, speculative finance, long-duration capital systems, and operating liquidity into a single institutional structure. The constitutional model rejects this arrangement. Agency 7 instead governs operating liquidity as a disciplined infrastructure system tied directly to stewardship authorization, covenant compliance, reserve capacity, and productive continuity.

Section 1 — Constitutional Purpose of Agency 7

The constitutional purpose of Agency 7 is the preservation of disciplined operating continuity throughout the community economy. Productive activity depends not only upon ownership structures and long-duration infrastructure, but also upon the continuous circulation of liquidity through inventories, suppliers, receivables, payroll systems, production cycles, operating contracts, and recurring commercial obligations.

The agency exists to ensure that authorized productive activity can function continuously once the constitutional acquisition and stewardship systems have completed their work. Agency 1 governs whether acquisition activity is authorized. Agency 7 governs the financing and liquidity systems that sustain those authorized operations afterward.

The constitutional model therefore treats operating liquidity as infrastructure rather than speculation. Agency 7 exists to preserve productive circulation while preventing operating finance from mutating into uncontrolled leverage expansion, speculative banking, passive deposit accumulation, or concealed insolvency structures disconnected from real productive activity.

Liquidity within the community is therefore governed primarily as flow rather than stored accumulation. The constitutional structure assumes that liquidity should circulate continuously through settlement, production, reserve allocation, contribution systems, supplier coordination, and productive operation rather than remaining dormant inside passive financial structures detached from stewardship activity.

Agency 7 therefore serves as one of the community’s principal operating circulatory institutions. Its purpose is not merely financial administration. Its deeper purpose is preserving disciplined productive liquidity throughout the community economy itself.

Section 2 — Short-Duration Asset Title Systems

Agency 7 governs title interests and collateral structures associated with short-duration productive assets throughout the community economy. These assets include raw materials, inventory, work-in-progress, accounts receivable, operating contracts, trade claims, cashflow assignments, and related operating instruments directly connected to productive activity.

The agency governs lien registration, encumbrance priority, collateral assignment, refinancing continuity, covenant enforcement, and the constitutional ordering of short-duration commercial claims. The constitutional significance of this structure lies in the fact that productive commerce depends upon continuously verifiable ownership and financing relationships. Inventory cannot circulate reliably if collateral claims become uncertain, hidden, or structurally ambiguous.

The constitutional structure intentionally separates these systems from long-duration capital governance. Agency 7 does not govern land title, buildings, permanent infrastructure, or durable capital equipment. Those systems remain constitutionally separated because the community intentionally distinguishes operating liquidity from permanent capital concentration.

The agency therefore functions as the constitutional title and collateral authority for the operating economy itself. It preserves clarity regarding ownership, refinancing continuity, collateral rights, and operating-credit relationships throughout productive commerce.

Section 3 — Working-Capital Financing Governance

Agency 7 governs the community’s revolving working-capital financing system. This includes the governance of operating credit facilities, refinancing systems, covenant structures, operating leverage rules, liquidity continuity standards, and revolving commercial-credit relationships associated with short-duration productive activity.

The constitutional model assumes that productive commerce naturally operates across timing gaps. Raw materials must often be acquired before products are sold. Contractors must be compensated before receivables settle. Inventory must circulate before revenue recognition occurs. Productive operation therefore requires revolving operating liquidity capable of bridging these cycles continuously.

The agency governs these financing systems only after constitutional authorization procedures are complete. TOK issuance through Agency 1 serves as one of the primary triggers for financing activation. Additional underwriting, insurance, lease, and operational validations are then completed through the appropriate constitutional agencies before financing execution proceeds.

Certified contractors subsequently execute the financing operations governed by Agency 7. The agency itself governs the standards, covenant structures, collateral systems, and liquidity framework within which those contractors operate.

Agency 7, therefore, does not function as a speculative credit generator. Its role is preserving disciplined, productive liquidity tied directly to authorized stewardship activity.

Section 4 — Exclusive Working-Capital Banking Structure

Agency 7 maintains the community’s exclusive external working-capital banking relationship. This relationship serves four primary constitutional functions. It clears and settles ordinary operating cashflows, hosts steward operating business checking accounts, provides the master revolving working-capital credit facility, and maintains the restricted constitutional tithing reserve system.

This banking relationship is intentionally narrow. The external bank does not function as a generalized consumer savings institution, speculative investment intermediary, or passive wealth-storage system. Its constitutional role is confined primarily to supporting productive operating circulation throughout the community economy.

The constitutional structure therefore rejects the ordinary modern banking arrangement in which speculative finance, household savings, consumer deposits, and productive operating liquidity become intermixed within a single institutional system. Agency 7 instead preserves a highly disciplined operating-credit architecture focused almost entirely upon productive flow and settlement continuity.

Liquidity within this structure functions primarily as governed circulation rather than passive stored balance. The operating economy is therefore designed around movement, settlement, and productive continuity rather than deposit accumulation.

Section 5 — Steward Operating Accounts and Near-Zero Balance Architecture

Each steward operates a single external business checking account connected to the Agency 7 operating system. The constitutional structure intentionally eliminates ordinary consumer deposit architecture.

Stewards do not maintain conventional savings accounts, idle deposit balances, certificates of deposit, or unrestricted passive cash reserves. Instead, the operating economy functions through near-zero idle balance architecture in which spending systems operate primarily as controlled sub-limits against constitutionally governed operating credit facilities.

This structure fundamentally changes the relationship between liquidity and accumulation. Modern financial systems frequently encourage large pools of passive stored cash disconnected from productive operation. The constitutional model instead assumes that liquidity should continuously circulate through settlement, supplier coordination, reserve allocation, production cycles, contribution systems, and operating activity.

The elimination of passive deposit accumulation also prevents the operating economy from gradually mutating into a speculative financial system driven primarily by idle balance multiplication rather than productive stewardship.

The steward operating account therefore functions primarily as a circulation node within the broader productive economy rather than as a passive wealth-storage mechanism.

Section 6 — Spending Instruments and Plan-Defined Credit

All steward spending systems operate against constitutionally governed operating credit structures. Cards, payment systems, dependent spending authority, and operating purchase mechanisms function as controlled sub-limits against the steward’s plan-defined revolving operating credit facility.

Dependents do not maintain separate personal banking systems. Their spending authority derives constitutionally from the stewardship operating structure itself. This preserves unified stewardship accountability while preventing fragmented consumer-debt structures from emerging throughout the community.

The constitutional structure intentionally connects spending authority to productive stewardship continuity. Consumption remains tied directly to sufficient, underwriting viability, covenant compliance, operational discipline, and broader stewardship planning systems.

This differs fundamentally from ordinary consumer-credit economies where spending frequently expands independently from productive operating capacity. Agency 7 instead preserves a structure in which liquidity remains continuously connected to stewardship accountability and productive viability.

The result is a community economy in which operating liquidity functions primarily as governed productive flow rather than unrestricted personal financial autonomy detached from stewardship responsibility.

Section 7 — Residue Recognition and Constitutional Sweep Systems

Agency 7 governs one of the community’s most important accounting structures: constitutional residue recognition and settlement sequencing.

Settlement follows a strict constitutional order. Operating obligations, supplier settlements, covenant requirements, contractor obligations, sufficient distributions, underwriting requirements, and recognized loss carryforwards must all be satisfied before residue recognition may occur.

Reserve obligations are then applied constitutionally prior to final residue determination. Only after these obligations are completed may final residue recognition occur.

Final residue is subsequently transferred through governed sweep mechanisms into Agency 7 as a plan-defined contribution rather than remaining as unrestricted idle deposit accumulation within passive personal banking systems.

This structure is constitutionally significant because it prevents residue from mutating into passive speculative liquidity disconnected from productive stewardship. Residue remains constitutionally “kept,” but it is kept through governed contribution structures rather than through unrestricted dormant accumulation.

The sweep system also prevents the creation of unintended trust liabilities within the broader operating structure. Liquidity continuously circulates rather than becoming trapped inside expanding pools of passive stored balances.

Section 8 — Agency 7 and the Restricted Tithing Reserve

Agency 7 governs the community’s restricted constitutional tithing reserve system. This reserve exists solely as a prefunded loss-absorption mechanism protecting the broader operating-credit structure from destabilizing failure exposure.

The reserve does not fund ordinary household sufficient. It does not stabilize personal lifestyle continuity, guarantee consumption levels, or preserve individual comfort. Its constitutional purpose is narrower and more structural. It exists solely to absorb operating-credit losses while preserving the constitutional principle that residue itself remains insulated from subsequent loss erosion.

The reserve is funded constitutionally as a mandatory quarterly operating expense equal to ten percent of the defined pre-residue surplus base after sufficient and after recognized loss carryforwards, but before final residue determination.

This sequence is constitutionally essential because the community intentionally prevents residue from functioning as a hidden operating-loss buffer. Losses must instead be recognized formally through the reserve system itself.

The reserve therefore functions as one of the community’s principal operating stabilization mechanisms because aggregate leverage remains constitutionally bounded by prefunded loss capacity rather than speculative collateral expansion alone.

Section 9 — Loss Absorption and Write-Off Procedures

The constitutional structure intentionally formalizes operating failure rather than concealing it indefinitely through refinancing, accounting abstraction, or speculative leverage expansion.

Reserve deployment may occur only under narrow constitutional conditions. Agency 5 must first initiate formal life-plan intervention or stewardship modification. Bureau VII must then conduct formal replanning through business-plan modification procedures documenting the restructuring or write-off process. Agency 21 underwriting systems must subsequently confirm continuing operational viability following restructuring.

Only after these constitutional procedures are complete may reserve funds be used for partial credit-line paydowns, charge-off offsets, or structured operating-loss absorption.

This structure preserves one of the community’s central constitutional principles: losses must remain visible. Insolvency may not be hidden indefinitely beneath perpetual refinancing systems or speculative accounting treatment.

Residue itself remains constitutionally insulated from ordinary operating-loss erosion after recognition. The constitutional model therefore forces formal recognition of operational failure within the governed restructuring framework.

Failure is therefore treated not as something to conceal indefinitely, but as something to recognize formally, restructure transparently, and govern constitutionally.

Section 10 — Credit Expansion Constraints

Agency 7 governs aggregate operating-credit exposure throughout the community economy. The constitutional structure rejects unrestricted leverage expansion based solely upon collateral valuation or speculative optimism.

Instead, aggregate operating leverage must remain bounded by the stressed-loss absorption capacity of the prefunded Agency 7 reserve structure. Expected stressed losses throughout the community must remain fully coverable through reserve capacity under adverse operating conditions.

Credit expansion is therefore constrained primarily by reserve resilience rather than collateral inflation alone. Operating liquidity may expand only when productive continuity and reserve capacity expand alongside it.

This creates a fundamentally different operating-credit structure than conventional banking systems. Modern leverage systems frequently expand through speculative asset inflation and continuous debt multiplication. Agency 7 instead constitutionally binds leverage growth to demonstrated productive resilience and prefunded loss capacity.

The result is a community economy that intentionally sacrifices unlimited leverage expansion in exchange for long-term operating durability and systemic stability.

Section 11 — Failure Recognition and Covenant Breakdown

Agency 7 governs the constitutional recognition of operating failure.

Failure occurs when a stewardship can no longer maintain plan-defined sufficient while simultaneously preserving covenant compliance under stressed operating conditions. Failure may also occur when TOK revalidation cannot be successfully completed following corrective intervention.

The constitutional structure intentionally rejects fictitious solvency preservation. The community does not indefinitely conceal operational deterioration through perpetual refinancing or hidden leverage expansion.

When constitutional failure occurs, restructuring, downsizing, replanning, liquidation, stewardship transition, or contractor replacement procedures begin openly within the governed constitutional framework.

Failure recognition therefore becomes one of the community’s stabilizing mechanisms rather than one of its greatest systemic fears. Because failure is recognized formally and governed transparently, deterioration becomes easier to contain before it spreads throughout the broader operating economy.

Agency 7 therefore contributes directly to long-term community resilience by preserving formal operational accountability.

Section 12 — Contractors, Banks, and Constitutional Separation

Agency 7 operates within a broader constitutional separation structure designed to prevent excessive concentration of authority.

Certified contractors execute financing operations after constitutional verification procedures are completed through the relevant agencies. TOK verification, lease validation, underwriting confirmation, insurance review, and business-plan authorization all occur through their proper constitutional authorities before financing execution proceeds.

The constitutional structure intentionally separates title governance, underwriting, insurance systems, liquidity provision, operational planning, land ownership, and contractor execution into distinct constitutional domains.

Lenders may hold liens and cashflow assignments within the Agency 7 collateral structure, but they do not govern the broader constitutional framework itself.

This separation prevents operating finance from consuming the remainder of the community’s institutional structure. Financial systems remain subordinate to constitutional governance rather than becoming the dominant organizing force of the community economy.

Section 13 — Agency 7 as the Circulatory System of the Community

Agency 7 functions as one of the community’s principal circulatory systems.

Just as biological circulation continuously distributes oxygen and nutrients throughout the human body, Agency 7 governs the continuous movement of productive operating liquidity throughout the community economy itself.

Inventory circulation, supplier settlement, receivable collection, payroll continuity, refinancing systems, trade liquidity, and productive coordination all depend upon these flows remaining stable and disciplined.

The constitutional model therefore treats liquidity as infrastructure rather than speculation. Agency 7 exists to preserve productive circulation while preventing the operating economy from collapsing into passive deposit accumulation, speculative leverage expansion, concealed insolvency, or uncontrolled financial fragmentation.

The agency ultimately governs movement itself. Its constitutional role is preserving the disciplined circulation of productive liquidity throughout the community so that stewardship continuity and productive operation remain stable across generations.

Section 14 — Conclusion: Agency 7 and Constitutional Operating Liquidity

Agency 7 governs one of the community’s most foundational operating systems: the constitutional management of short-duration productive liquidity.

Through working-capital governance, revolving financing systems, collateral administration, covenant enforcement, residue recognition structures, reserve management, and operating-liquidity circulation, the agency preserves the continuous flow necessary for productive community life itself.

The constitutional structure assumes that communities become unstable when liquidity becomes detached from productive stewardship, when leverage expands beyond reserve capacity, when insolvency remains hidden indefinitely, or when deposits accumulate passively outside productive circulation.

Agency 7 exists to prevent these outcomes.

The agency therefore serves as one of the principal guardians of constitutional operating continuity within the broader community structure. Through disciplined liquidity governance, reserve-bounded leverage systems, constitutional settlement sequencing, and rule-bound operating finance, Agency 7 helps preserve a productive community economy grounded in stewardship continuity rather than speculative abstraction.