Agency 7: Community Bank

The Community Bank Agency is the seventh agency in the community. It is the first agency in the Economic Bureau. Other agencies in the bureau are Capital Bank Agency (agency 8), and the Commercial Bank Agency (agency 9). I

The agency provides personal banking services to all participants. The agency also provides banking services and loans to all agencies in its “column” a grouping of 8 agencies that align in terms of their functions.

The Community Bank Agency receives funds in the form of investment from the Capital Bank Agency (agency 8), which it then uses for its operations, including capitalizing the loans it offers, and other chargeable services to participants. From the revenues the agency generates, it is able to honor its obligations, including paying a return to the Capital Bank for capital invested. The agency is therefore geared to run on a profit, while delivering quality and affordable services.

The Economic Bureau is the community’s repository. It stores the community’s resources and leverages them to enhance access, and to enable the community to derive maximum benefit. The bureau forms the core of the community econosystem, which anchors the community’s aim of providing sustainable prosperity for all.

What does the bank do?

As the community’s retail banker, and as part of the Economic Bureau, the Community Bank’s roles help in creating money, ease the movement of funds, and support personal transactions transactions. The agency:

- Holds participants’ checking and savings accounts

- Provides commercial loans to agencies in its vertical

- IP ownership

Retail banking

The Community Bank Agency provides participants with ordinary retail banking services through the checking and savings that they hold with the bank. Participants access these services online, without having to interact with the bank’s agency presidency.

The Community Bank is the primary banker for participants. While they have business accounts with the Commercial Bank Agency (agency 9), their accounts there are mostly to facilitate business transactions. The funds in their business accounts are transferred from their checking and savings accounts as needed from time to time.

The bank’s system enhances commerce in the community by speeding up the movement of funds. It also maintains sophisticated algorithms that help participants set what they need in their checking and savings accounts and term deposits.

Movement of funds

In the course of their businesses, participants deposit some profits from their businesses in their checking accounts. A checking account is designed to take care of frequent personal needs, such as food, personal care items, and rent. In the course of a participant’s business, the funds in their business account may be insufficient to handle a business expense. In such instances, any balance is obtained from the participant’s checking account.

The bank’s algorithm considers a participant’s personal and contingent business needs and sets a minimum amount it deems sufficient to cover them for a specific period. The algorithm also considers the frequency of transactions in the account. Therefore, each participant has a specific amount that the algorithm retains in the checking account.

When the set limit for deposits in the checking account is reached, the system automatically transfers any surplus to the participant’s savings account. Further deposits within the specified period are directly transferred to savings. Funds in the savings account also have a ceiling. In setting this ceiling, the algorithm considers medium-term potential needs that a participant may face. It considers, for instance, their health, dependents, education needs, and business health, among others. Savings accounts earn an interest, based on average amounts and the Community Bank’s performance.

| Checking account | Savings account | Term deposit |

|---|---|---|

| Short-term personal expenses including food, personal effects, and possible business costs | Anticipated, significant, expenses including medical bills, business expansion, education | instrument to save up to buy additional partnership interest in Capital Bank |

As a participant’s business prospers, and saved funds reach the specified amount, the bank’s algorithm transfers the excess to term deposits. Terms deposits earn interest as well, based on the same parameters as savings. Term deposits are held until they reach $30,000, after which 20,000 is transferred to the Capital Bank and added to the limited partner’s partnership interest. Term deposits are not held to mature at a specific time, such as a month or quarter, but mature when they reach $20,000, including interest. This process is repeated over and over, as a participant prospers in the economy.

If a participant is still a minor dependent, they can still accumulate their term deposits. If these deposits hit $20,000 the dependent can become a limited partner on reaching 16 years of age, at which point $20,000 or more, in multiples of 20,000, from their term deposit is transferred to the Capital Bank. The algorithms also help the bank control withdrawals and transfers, a crucial element in the bank’s strategy of improving its resilience and stability, while averting bank runs.

While money in checking and savings accounts can freely be withdrawn as needed, term deposits have a withdrawal limit of 2% per day. Any withdrawals above 2% need approval from the agency presidency, on advice from the village presidency for human relations that serves the account holder. The limit protects the bank from potential bank runs that can destroy them. The limit also gives the Community Bank greater room to use depositors’ money when providing loans to agencies, thereby enhancing the utilization of financial resources and enhancing productivity.

Providing banking services to villages and agencies

Each agency in the community has a bank account with the bank agency in their column. At the same time, each village and district presidency has a bank account with the bank agency under which the agency they serve falls. Agencies’ bank accounts are operated by the relevant agency presidency. Respective village and district presidencies operate their districts’ accounts as applicable.

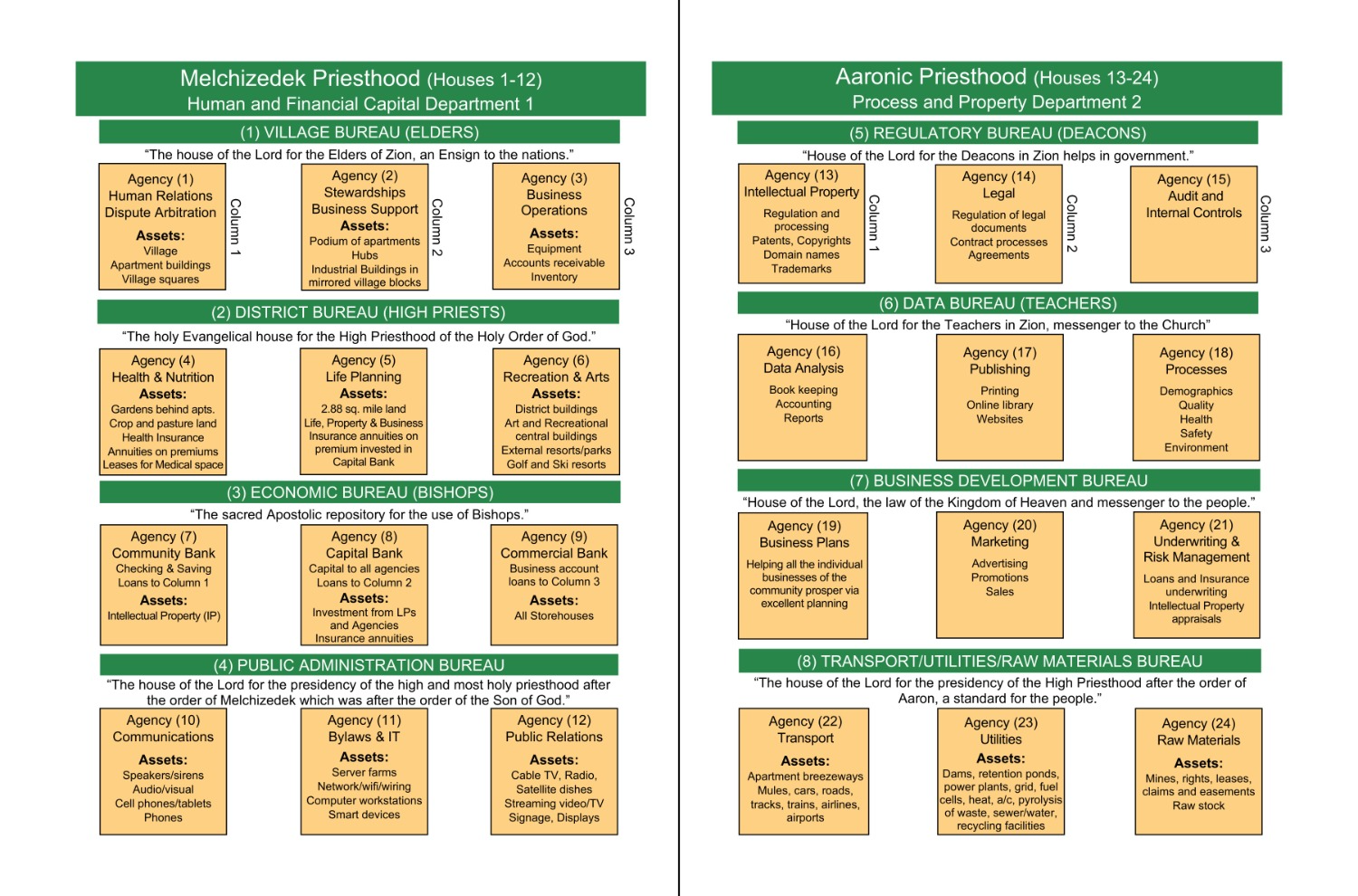

| Agencies banking with Community Bank (agency 7) | Agencies banking with Capital Bank (agency 8) | Agencies banking with Commercial Bank (agency 9) |

|---|---|---|

| Residential and Mediation (agency 1) | Commercial (agency 2) | Enterprise Assets (agency 3) |

| Health and Nutrition (agency 4) | Life Planning (agency 5) | Sports, Arts, and Leisure (agency 6) |

| Communication (agency 10) | Governance, IT, and Security (agency 11) | Media and Public Engagement (agency 12) |

| Innovation and IP (agency 13) | Legal (agency 14) | Audit and Oversight (agency 15) |

| Accounting (agency 16) | Publishing and Teaching (agency 17) | Metrics (agency 18) |

| Business Planning (agency 19) | Marketing (agency 20) | Underwriting (agency 21) |

| Transport (agency 22) | Utilities (agency 23) | Raw Materials (agency 24) |

In the villages and districts, presidencies access banking services as follows:

| Village/ District presidencies banking with Community Bank | Village/ District presidencies banking with Capital Bank | Village/ District presidencies banking with Commercial Bank |

|---|---|---|

| Village presidency for residential and mediation | Village presidency for Commercial | Village presidency for enterprise assets |

| District presidency for health and nutrition | District presidency for life planning | District presidency for sports, arts ,and leisure |

Villages, districts, and agencies receive the capital they need to start up and run their operations from the Capital Bank Agency. When any of the entities that bank with the Community Bank needs a loan, it gets the required down payment from the capital. Down payment limits the bank’s risk exposure and allows villages, districts, and agencies to participate in the acquisition of assets.

Community Bank loans are used to acquire assets that are then leased out to participants at a fee. The revenue collected is used to pay back loans, and the return due on the capital invested by the Capital Bank. All assets acquired by villages and districts are ultimately owned by their agency.

The Community Bank does not provide participants with commercial loans. This is based on, among other things, the fact that participants do not need to own any assets in the community besides their business, which they are helped to build through the lease/ factoring of space, inventory, and equipment from the village agencies. In other words, the absence of the opportunity to own personal assets negates the need to access a loan.

IP ownership

The community maintains an aggressive innovation posture, facilitating and encouraging participants to focus on research and development, as well as an education system geared towards education. The community also The Innovation and IP Agency (agency 13) helps participants by giving them advice, connecting them to participants, and processing Ip claims.

Once an IP has been successfully filed in the community and with the relevant authorities, it is regarded by the community, as is standard accountiing practice, as a form of capital, and an asset.

In pursuant to the principle of “all things in common,” all assets and forms of capital are owned by the capital. While the innovator retains the first right of refusal to an IP, it now becomes the property of the Community Bank Agency.

The agency, by presenting the IP as a part of capital, is able to create loans based on it. This leverages the value of the IP, increases the bank’s lending capacity, and therefore further magnifies the value of the IP.

While it owns the IP, the Community Bank does not engage in licensing activities. These are the role of the Innovation and IP Agency.

Banking and loan-making characteristics

In modern practice, commercial banks issue loans while adhering to their exposure to risk, as well as their ability to sufficiently meet customer demands, such as withdrawals. Banks typically apply the leverage ratio, and the capital adequacy ratio when calculating how much in loans they can issue, and the level of deposits needed to deal with operations, including meeting depositors’ obligations.

The capital adequacy ratio is a percentage of loans (risk-weighted assets) that a bank should have as capital. An international regulatory framework for banks known as Basel III has set this at 10.5%. This means that of the total loans that a bank makes, it needs to weigh the risk, and then have at least 10.5% of that in capital.

Typically, the community will have low risk due to the stability offered by the economic system, the access to near-perfect and well-analyzed information, and the absence of unsecured loans to individuals. Therefore, a loan of $1,000,000 issued to an agency might be risk-weighted to $100,000. The bank would be required to have 10.5% of this ($10,500) as capital.

Since the Community Bank would be subject to regulatory guidelines in the area where a community is located, it would need this capital, which it obtains from the Capital Bank. The Capital Bank’s investment in the Commercial Bank is therefore an important determinant of how much in loans the commercial bank can advance.

The second measure, leverage ratio, refers to a bank’s tier 1 capital divided by its assets. Tier 1 capital for the Commercial Bank is the investment received from the Capital Bank. This is divided by assets, including loans, and, in this case, any other assets it holds.

Creating money

the Commercial Bank creates money through the loans it issues to agencies and villages. The bank has a monopoly in banking services. Therefore, when it issues a loan, the arising deposit is banked with it, which, before the loan was created, did not exist. The new money can be used to back another loan, and so on, through a model known as fractional reserve banking. Through its activities, the bank can control the flow of money in the economy, increasing supply, tackling inflation, and spurring economic activity.

The reserve ratio is used to approximate the limit to which a bank can multiply or create new money. The money multiplier is defined as:

| money multiplier = | 1 |

| reserve ratio |

Using the Basel rate (10.5%), this can be calculated as:

| money multiplier = | 1 | = 9.524 |

| 0.105 |

This measure implies that through fractional reserve banking, the bank can multiply money (or increase the money supply in the economy) by more than 9 times.

The NewVistas banking system

The Community Bank will be able to leverage capital and deposits by up to 100 times. The bank will be able to achieve this through aspects of the community’s architecture, as well as its automated system, as detailed below.

First, the community requires that every participant in the community be banked. The Community Bank works with other agencies to support a cashless economy. These two aspects have the effect of putting all financial resources in the system at all times and eliminating leaks and capital hoarding, which are consistent with cash-based systems and inadequate access to banking (resorting to alternative methods of banking). As a result, more resources are at the bank’s disposal.

Secondly, limits on the withdrawal of savings, besides preventing bank runs, put additional funds at the disposal of the Community Bank. The bank can plan after forecasting what it will be able to lend, and having a reasonable estimation of how much money will be withdrawn and deposited over a period.

Thirdly, most loans advanced by the bank are spent on real physical assets that have already been rented out, guaranteeing an income that will be used to repay the loan. This greatly minimizes or even eliminates the risk associated with the nonperformance of loans. The business plans that occasion the loans are prepared with the help of near-perfect, updated information, which greatly enhances their chances of success.

The investment options that the loans are directed to are widely diversified. Agencies, villages, and districts use loans to acquire buildings, equipment, raw materials, and educational and sports facilities, among others. They are never issued to individuals, eliminating the chances that loans could be diverted to unintended uses.

How the agency works

Background on presidencies

Every presidency in the community presidency is a four-member entity whose members serve and represent one of the four major demographic groups, known as divisions: partnered males (A), partnered females (B), single females (C), and single males (D).

These four major demographics are evenly split in ordinary society, with each group accounting for between 23 and 27% of the population, and with regular fluctuations as people’s status changes. The community appreciates that discrimination across all social categories happens based on people’s status as single or partnered, other social categorizations notwithstanding; partnered males are likelier to dominate other demographics, especially single males and single females. Partnered females are also likelier to have better outcomes in careers and leadership than single females.

The community’s infrastructure promotes equal access to economic and social resources and opportunities. The composition of the community as a whole and those who serve it in the community public service is closely monitored to prevent numerical domination, which can lead to nepotism or unequal access.

The recruitment to be a participant, and to serve in the public service carefully considers other social categorizations, to ensure racial, ethnic, religious, and sexual groups are well represented in the community as they are in the society in which a community operates. These considerations inform the constitution

Agency presidency, bureau board, and demographic presidencies

The Community Bank Agency is served by an agency presidency, comprised of 4 presidents from four divisions, which handles strategy formulation and adjustment, as well as formulating and communicating operational procedures for the agency. Additionally, the presidency also facilitates the setting up of the agency’s automated system and adjusts it as necessary to better achieve its goals.

As part of the Economic Bureau, the agency presidency forms a bureau board with agency presidencies serving the Capital and Commercial Bank agencies. The board acts as a check and monitoring tool for individual presidents and agencies, especially when decisions have far-reaching implications for the community.

Within the bureau board, three presidents from the same demographic form a demographic presidency. There are four such presidencies in the bureau. The demographic presidency works on matters of common interest to a demographic, that cut across the three agencies. The demographic presidency also plays an important role in the mentorship and training of new presidents.

| Demographic presidency A | Demographic presidency B | Demographic presidency C | Demographic presidency D | |

|---|---|---|---|---|

| Agency presidency, Community Bank (7) | 7A | 7B | 7C | 7D |

| Agency presidency, Capital Bank (8) | 8A | 8B | 8C | 8D |

| Agency presidency, Commercial Bank (9) | 9A | 9B | 9C | 9D |

Limited partners and branch presidencies

Limited partners and dependents

A limited partner is the basic unit in the community. A limited person, usually above 18 years old, but sometimes as young as 16, has been admitted into the community and has invested $20,000 as partnership interest, for which they earn a return. This is regarded as one unit of partnership interest.

Over time, a limited partner can add more units of partnership interest, as their business prospers. The more partnership interest units a limited partner has, the more the return they receive from the Capital Bank.

A dependent is a minor, or a person living with a disability, under the care of a limited partner. In some instances, a dependent may be a fit adult, who for various reasons is supported by community agencies, and assigned by contract to a limited partner. Limited partners are responsible for any legal agreements that their dependents enter into, either with community agencies or other participants, and therefore have the right of attorney.

Together, limited partners and dependents are referred to as participants. Participants who are dependents, because they are still minors, can start a business when they reach 12 years of age. This allows them to save up and invest $20,000 into the community by their 18th birthday, and possibly as early as 16.

Limited partners and their dependents reside in apartments (village buildings). Each apartment has 4 floors, with each floor containing 16 apartments. Each floor has floor has 7 – 12 limited partners, with each limited partner having 1 – 3 dependents. Each floor therefore has around 25 residents. With four floors, each building has approximately 100 residents. An apartment building also forms a branch.

Limited partners and unit

A limited partner is the basic unit in the community. A limited partner, usually above 18 years old, but sometimes as young as 16, has been admitted into the community and has invested $20,000 as partnership interest, for which they earn a return from the Capital Bank Agency, which invests other community agencies. This is regarded as one unit of partnership interest. Over time, a limited partner can add more units of partnership interest, as their business prospers. The more partnership interest units a limited partner has, the more the return they receive from the agency.

A dependent is a minor, or a person living with a disability, under the care of a limited partner, and who has, in any of these cases, given their power of attorney to the limited partner. In some instances, a dependent may be a fit adult, who for various reasons is supported by community agencies, and assigned by contract to a limited partner. Limited partners are responsible for any legal agreements that their dependents enter into, either with community agencies or other participants. Together, limited partners and dependents are referred to as participants.

Participants who are dependents, because they are still minors, can start a business when they reach 12 years of age. This allows them to save up and invest $20,000 into the community by their 18th birthday, and possibly as early as 16. Limited partners and their dependents reside in apartment buildings (village buildings). Each apartment building has five floors, with four containing apartments. An apartment building also forms a branch.

Captains and branch presidencies

Of the approximately 100 residents in a branch, around 40 of them are limited partners.They are divided into 4 units, each of which has 10 limited partners and their dependents. The limited partner membership in a unit is diverse, containing different social groups that are reflective of the society within which a community operates.

Additionally, a unit contains members of the four main demographics: partnered males (A), partnered females (B), single females (C), and single males (D).

The 4 demographics in the branch form 4 groups, as follows:

- Group 1: partnered males and females

- Group 2: single females and males

- Group 3: partnered and single males

- Group 4: partnered and single females

Within each group, there are different subsets, known as classes, based primarily on age. There is a class for Nursery (0-2), toddlers (3 – 5), young children (6-9), pre-teens (10-12), teens (13-18), young adults (19-31), adults (32-72), and empty nesters (73+).

| Meeting week | Class 1 | Class 2 | Class 3 | Class 4 | Class 5 | Class 6 | Class 7 | Class 8 |

| Week 1 and 3 | All partnered adults | All single adults | Teen boys and girls | Pre -teens | Young children | Toddlers | Nursery | |

| Week 2 and 4 | All males | All females | Teen boys | Teen girls |

Further details on the composition of units, groups, classes, and branches, and their meeting schedules, is detailed here.

Recruitment and diversity

Captains are responsible for recruiting limited partners into the community through their council and by extension, branch. A captain does not recruit limited partners only from their demographic. Instead, they work to ensure that their recruits are diverse, considering social categorizations, gender, and social status, in addition to demographic groups.

Captains work in concert with their fellow captains in the branch presidency, and other presidencies in a village and district to ensure that the district is as diverse as possible. They are guided by present data on how diverse their district, village, and branch are, and what needs to be focused on to improve. They are also guided by community bylaws, which expressly require diversity as shown by demographic data about a population from which the community intends to recruit limited partners.

The captain serves as a service extension of the Human Relations Agency, though they also act as an interface between participants and other community agencies. For agencies that do not have operational presidencies, such agencies in the Economic and Public Administration Bureaus, captains come in handy in helping participants navigate these agencies’ automated system and other relevant tools used by the agency to deliver services.

The automated system is designed to help participants with all the help they need in matters related to various agencies, including the Human Relations Agency. However, should they run into problems, captains assist them in navigating the system, or direct them to relevant contractors who help them at a fee. at a fee.

Automated system

For most of its duties, especially those that involve interaction with participants, the Community Bank works through an automated system. The automated system helps participants open and maintain bank accounts. The automated system is critical in helping participants move funds through various accounts (checking, savings, term deposits, and finally, partnership interest). It also works with agencies, districts, and villages for their banking needs.

Contractors

The Community Bank relies on contractors to handle aspects of its operations that the automated system, agency presidency, and branch presidencies cannot handle. Contractors develop the automated system. The agency also hires contractors to help in developing strategies and operational policies, and to monitor implementation as necessary.

Participants can also hire contractors to assist them in navigating the automated system. In addition, contractors working as financial professionals can help participants make better financial decisions and enable them to make the most of the community’s economic model.

Inter-agency cooperation

The 24 community agencies form three columns of 8 agencies each. There is loose collaboration between the agencies in a column. The Community Bank Agency is part of the first column.

The Community Bank Agency issues loans to all agencies in its column. The agency collaborates with the Cropland and Pastures Agency to ensure that all produce is well stored in the mirrored storehouse. The bank also works with Business Planning (agency 19) and IP (agency 13) to encourage the drawing up of quality business plans, and facilitation for businesses and innovators.

Presidencies’ offices, meetings, and quarterly conferences

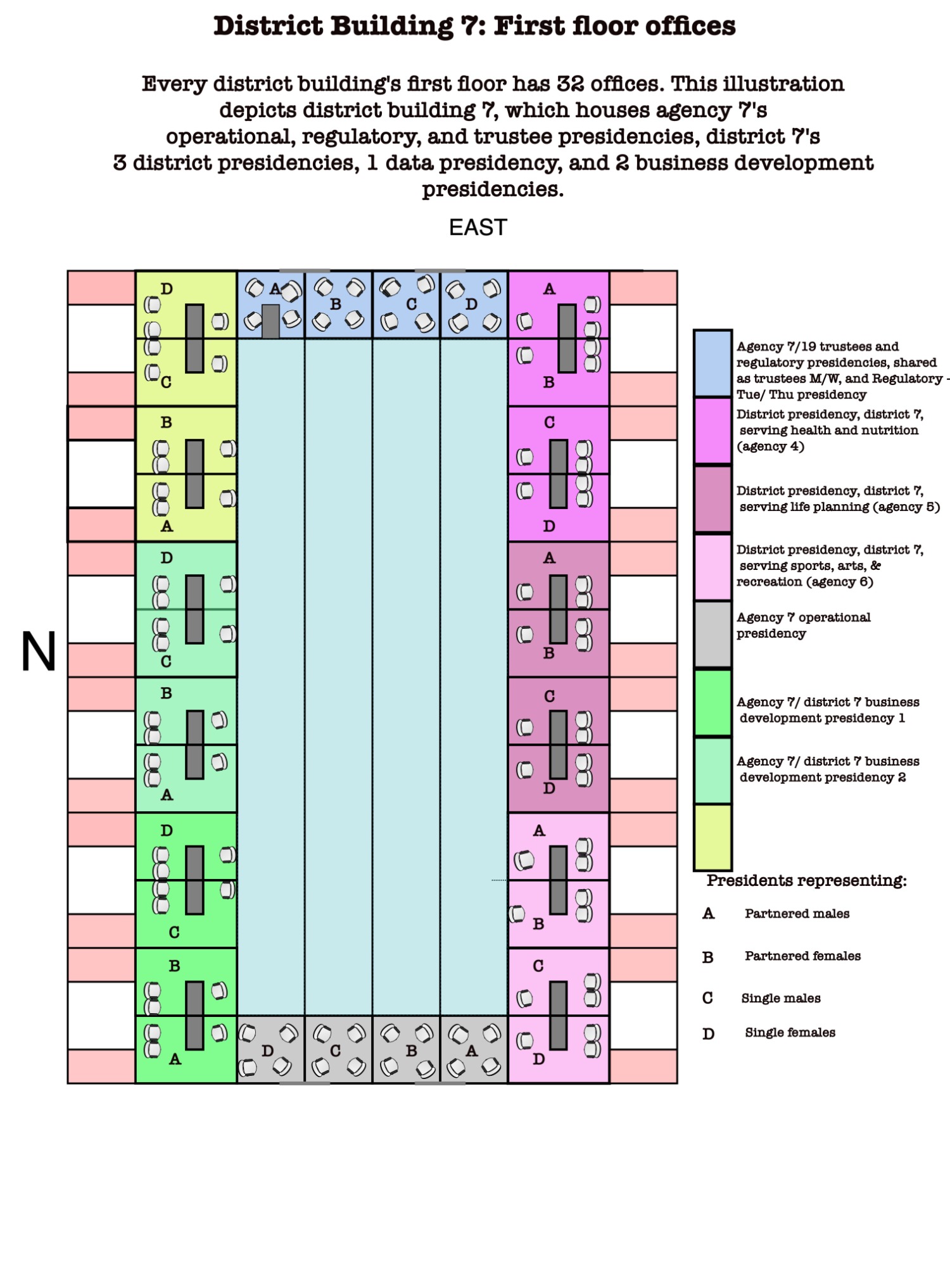

Offices

The Community Bank Agency presidency has permanent dedicated offices in District Building 7’s first floor, on the western side. Facing them on the eastern side are the offices for trustee presidency and Regulatory Bureau’s operational presidency serving the agency and District 7.

Trustees and the regulatory operational presidencies alternate their offices. Trustees have the offices in building 7 on Mondays and Wednesdays, while the operational presidencies use the offices on Tuesdays and Thursdays, as shown in this timetable:

| Building 7/ Community Bank | Building 19/ Business Planning | |

|---|---|---|

| Monday | Trustee presidency | Regulatory Bureau presidency |

| Tuesday | Regulatory Bureau presidency | Trustee presidency |

| Wednesday | Trustee presidency | Regulatory Bureau presidency |

| Thursday | Regulatory Bureau presidency | Trustee presidency |

The first floor’s layout is as follows, including other public servants who serve District 7.

Working hours and meetings

Agency presidents, trustees, and regulatory agency presidents work in their offices on a full-time basis. To allow for this, they are required to be at least 50 years of age, be experts in NewVistas concepts, an be semi or fully retired from their business. This allows them to dedicate much of their productive time to serving the community.

Other presidencies work from Monday to Thursday, from 8 – 8:45 AM. their offices are converted for this purpose, and can thereafter be used for other activities, such as office space for participants, hotel rooms and hospital consultation rooms. On Thursday, each presidency (four presidents serving A, B, C, and D) meets for a 45-minute meeting from 9:00 to 9:45 in the morning.

On the last Friday of each quarter, between 9:00 AM and 12:00 PM, each demographic presidency meets. The three-member presidency discusses common bureau matters that are of interest to the demographic they serve. On Saturday, again between 9:00 AM and 12:00 PM, the whole board meets, where the presidents present their input from the previous day’s demographic presidency meeting, and prepare for the quarterly conference. The aim is to have a cohesive presentation during the quarterly conference but tailored to specific demographic interests.

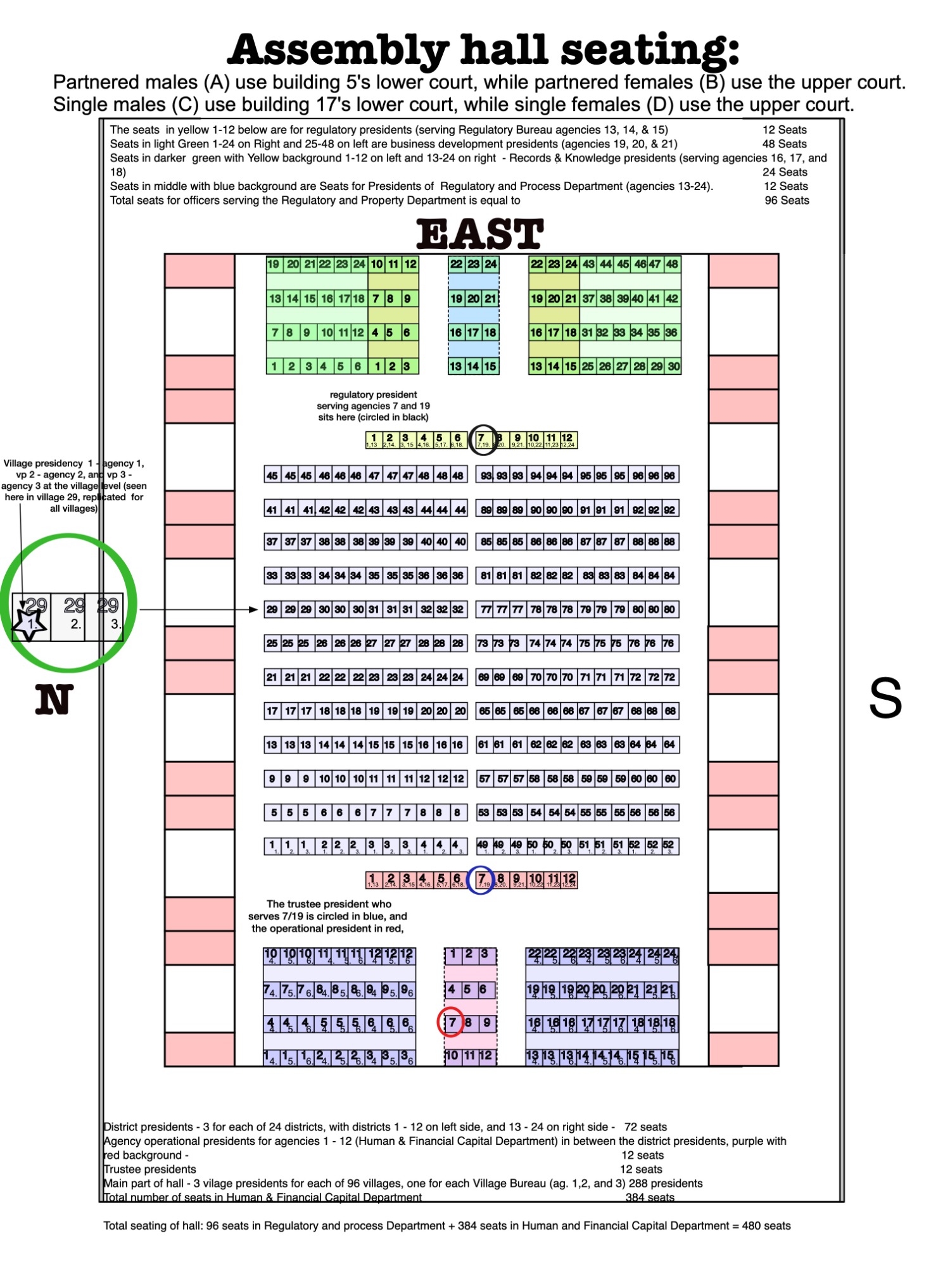

Quarterly conferences

Quarterly conferences are held on the last Sunday of each quarter, from 9:00 AM to 3:00 PM, with a lunch break in between. During quarterly conferences, each demographic presidency sits together in the same row.

Quarterly conferences are held in District Buildings 5 and 17. Each building has a lower and higher assembly court. The different demographic groups use the assembly courts as follows:

| Building | Assembly court | Demographic |

|---|---|---|

| 5 | Lower court | Partnered males (A) |

| 5 | Higher court | Partnered females (B) |

| 17 | Lower court | Single females (C) |

| 17 | Higher court | Single males (D) |

Branch presidencies do not attend quarterly conferences. Instead, they follow the relevant proceedings online alongside other participants.

Each of the four assembly courts has seats for 480 presidents representing the respective demographic. In the diagram below each of the 4 courts is illustrated. The ceiling of each court has an elliptical arch that enables agency presidents, who are the only ones who make a presentation during the conference, to speak without the need to amplify their voices. The 480 seats are easily rotatable to enable presidents to face whoever is speaking.

Each of the four courts has an identical arrangement and number of seats. The exact arrangement of each court can therefore be illustrated using one court, in this case, building 5’s lower court that is used by partnered males (A).

Within an assembly court, the 480 presidents are arranged in terms of demographic presidencies of 3. The Economic Bureau’s demographic presidency for partnered males (7A, 8A, and 9A) sits in the highlighted seats. Various district demographic presidencies also sit on the same row.

[1] These demographic groups are partnered males (A),partnered females (B), single females (C), and single males (D).