Agency 8: Capital Bank

The Capital Bank is the eighth agency in the community. The Capital Bank Agency is part of the Economic Bureau, which anchors the community’s economic system. Other agencies in the bureau are Community Bank (agency 7) and Commercial Bank (agency 9).

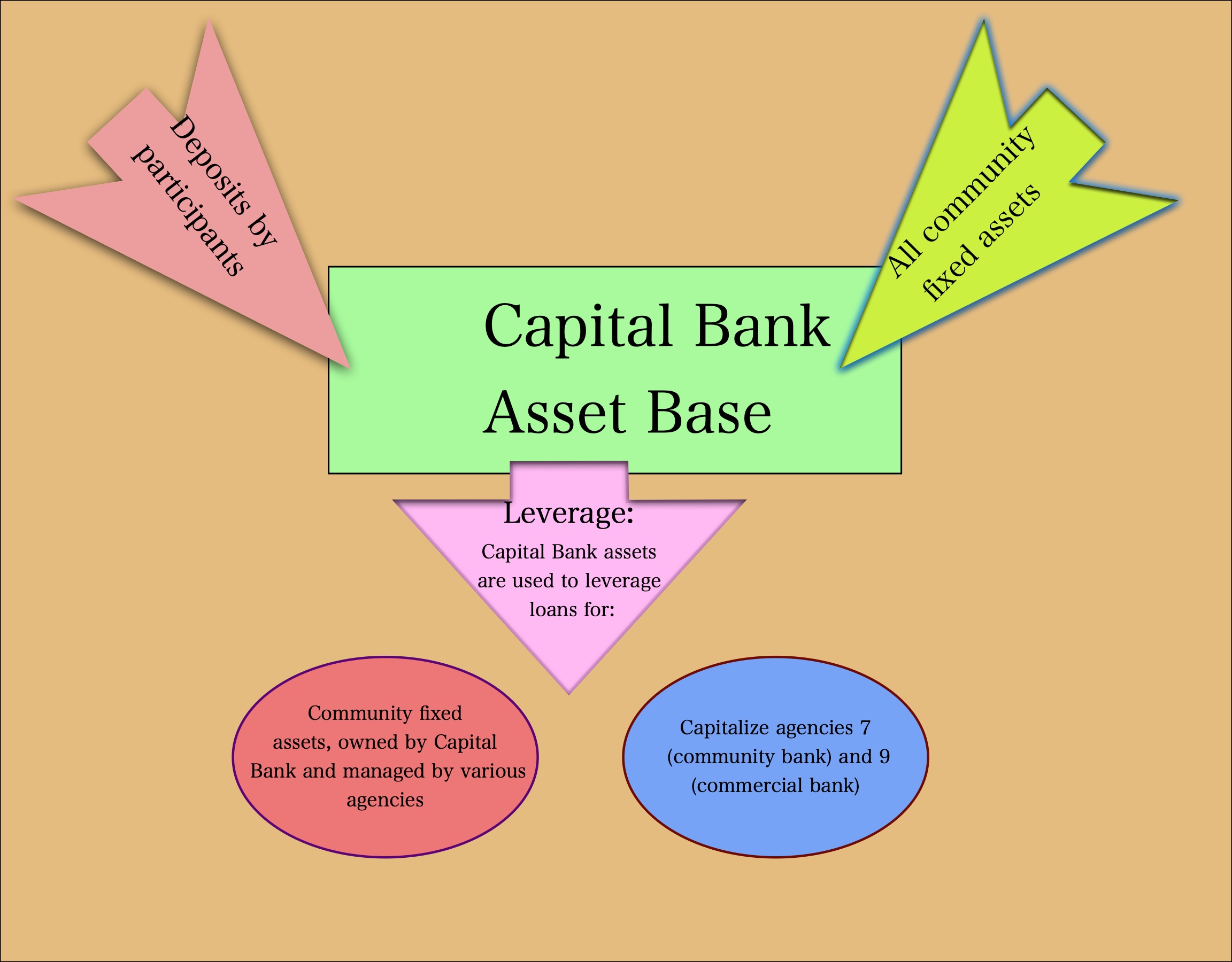

The Economic Bureau is critical in leveraging community assets, including fixed deposits by participants, and providing agencies with the necessary fixed assets and infrastructure. As the community’s repository, the Economic Bureau receives, stores, and provides ways of utilizing resources that result in social and economic prosperity.

When limited partners join the community, they deposit a minimum of $20,000, which is held by Capital Bank Agency. The agency uses these funds to acquire fixed assets, which agencies use to offer services to participants.

{kind=link}

Roles of the Capital Bank Agency

The Capital Bank Agency performs a number of roles to support the community’s economy and ensure optimal utilization of limited partners’ deposits and community fixed assets.

- Receiving limited partners’ joining and fixed deposits

- Capitalize banks to offer loans

- Acquisition of fixed assets

Receipt of limited partners’ deposits

When limited partners join the community, they deposit their net worth, either immediately, or over a period of three years as they liquidate their fixed properties, into the Capital Bank. At the time of formally joining, a limited partner must deposit at least $ 20,000 in the bank.

Limited partners are encouraged to continually depoosit their net worth in the Capital Bank as their business prospers. Each 20,000 deposit is considered one unit.

In return, the bank offers the limited partner a clearly detailed certificate, which clearly states its responsibilities to the depositor, including a guaranteed 12% annual return, and the ability to use the deposit as collateral for loans from other bank agencies. The more units a limited partner has, the more the return they earn.

The depositor also has a set of responsibilities to the bank, including an undertaking to withdraw no more than 2% of their total deposits in the bank in a month. The deposit certificate is motivated by the need to have participants’ absolute trust in the system, and is inspired by the LAW revelation given to Joseph Smith in 1831, which directed that saints who “consecrated” their properties would receive a “deed and covenant which cannot be broken.”

Investing funds

On receiving limited partners’ partnership interest, the Capital Bank has the responsibility of finding the right investment options to put the funds. In selecting investment options, the bank considers risk and return. Most of the capital invested in the bank is in turn leveraged in loans to acquire fixed assets.

The Capital Bank invests limited partners’ deposits in community agencies. Agencies use these funds for operational expenses. A significant portion of operations expenses is taken up by hiring contractors to develop agencies’ automated systems, rent, and as a down payment for loans to develop or acquire assets.

Some other investments, though making solid economic sense, are done so that the community can function as intended in the plat. Among others, it must have sufficient land for the physical campus, industrial blocks, cropland, and wilderness. It also needs to put up buildings, breezeways, easements, and all other physical infrastructure. The community also needs connectivity and equipment.

The Capital Bank facilitates the acquisition of these resources by issuing loans to itself. Agencies are responsible for acquiring the resources and managing them, but they appear in the Capital Bank’s balance sheet as its assets, and are therefore both used as a collateral in loans, and as capital to leverage in creating loans.

While managing the resources acquired with the Capital Bank’s facilitation, agencies are run as a business and are expected to make a profit. From the profits, they pay the bank a fee, which the bank considers a return as the investor. Agencies are therefore not burdened with capital intensive acquisitions and loan repayments, and can focus more on quality service delivery.

While the Capital Bank owns the various fixed assets, other agencies are responsible for maintaining the assets to be in a good condition, and even advising the bank on newer, better alternatives, and disposal at the end of an asset’s life.

Capital to bank agencies

A significant amount of the capital that the Capital Bank invests in community agencies is earmarked for the two banks – Community Bank and Commercial Bank. The banks use this money to create loans to villages, districts, and agencies. As with funds invested in other agencies, the Capital Bank receives a return on its investment from the banks.

The Community and Commercial Banks also have other sources of capital which they use to create loans. For instance, the Community Bank owns all current assets including accounts receivable, inventory, and raw material. The Commercial Bank owns all intellectual property (IP) originated by participants. By consolidating all assets in the hands of the three bank agencies, the community has the ability to leverage these assets, including participants’ deposits, at much higher levels than in contemporary banking practice.

To a significant extent, the Capital Bank determines the amount of loans that the Community and Commercial Bank agencies can lend. By controlling how much it invests in the bank agencies, the bank controls a part of their capital adequacy ratio. It can therefore help to manage the community’s economic trends.

How the agency works

Background on presidencies

Every presidency is a four-member entity whose members represent one of the four major demographics, known in the community as a division: partnered males (A), partnered females (B), single females (C), and single males (D).

These four major demographics are evenly split in ordinary society, with each group accounting for between 23 and 27% of the population, and with regular fluctuations as people’s status changes. The community appreciates that discrimination across all social categories happens based on paeople’s status as single or partnered, other social categorizations notwithstanding: partnered males are likelier to dominate other demographics, especially single males and females. Partnered females are also likelier to have better outcomes in careers and leadership than single females.

The community’s infrastructure promotes equal access to economic and social resources and opportunities. The composition of the community as a whole and those who serve it in the community public service is closely monitored to prevent numerical domination, which can lead to nepotism or unequal access.

The recruitment to be a participant, and to serve in the public service carefully considers other social categorizations, to ensure racial, ethnic, religious, and sexual groups are well represented in the community as they are in the society in which a community operates. These considerations inform the constitution of these presidencies.

Even though presidents represent a specific demographic, they serve the whole community. Therefore, their identification with a demographic is purely for the purposes of representation.

Agency presidencies and council, bureau council, and demographic presidencies

The Capital Bank Agency is served by three agency presidencies – operational, trustee, and regulatory. Each presidency, comprised of 4 presidents, has a specific role in the agency. Trustees, who also serve agency 20 (Marketing), originate strategy, and are the agency’s legal representatives.

Operational agency presidencies, after consultations with other agency presidencies in the agency, implement strategy. The operational agency presidency mostly works through the automated system, whose set-up and operation it manages.

Both trustees and operational agency presidencies are monitored and guided on compliance by the regulatory agency presidency. The regulatory agency presidency, like the trustee presidency, also serves the Marketing Agency in the same capacity.

Together, the three agency presidencies create an agency council. The council, after the trustees originate strategy, delibertes and adopts it as desired, and monitors implementation. The council is a useful check and balance to individual presidents’ performance. the council is especially important when decisions have far-reaching implications for the community.

Alongside those serving the other two agencies in the Economic Bureau, the operational agency presidency belongs to a bureau council. The council is collaborative and endeavors to train, mentor, presidents, while discussing issues that require a coordinated approach from the bureau.

Within the bureau council, three presidents from the same demographic form a demographic presidency. There are four such presidencies in the bureau. The demographic presidency works on matters of common interest to a demographic, that cut across the three agencies. The demographic presidency also plays an important role in the mentorship and training of new presidents.

| Demographic presidency A | Demographic presidency B | Demographic presidency C | Demographic presidency D | |

|---|---|---|---|---|

| Agency presidency, Community Bank (7) | 7A | 7B | 7C | 7D |

| Agency presidency, Capital Bank (8) | 8A | 8B | 8C | 8D |

| Agency presidency, Commercial Bank (9) | 9A | 9B | 9C | 9D |

Limited partners and branch presidencies

Limited partners and dependents

A limited partner is the basic unit in the community. A limited person, usually above 18 years old, but sometimes as young as 16, has been admitted into the community and has deposited $20,000 as partnership interest, for which they earn an interest, usually fixed at 12%. This is regarded as one deposit unit.

Over time, a limited partner can add more units as their business prospers. The more deposits a limited partner has, the more the interest they receive from the Capital Bank.

A dependent is a minor, or a person living with a disability, under the care of a limited partner. In some instances, a dependent may be a fit adult, who for various reasons is supported by community agencies, and assigned by contract to a limited partner. Limited partners are responsible for any legal agreements that their dependents enter into, either with community agencies or other participants, and therefore have the right of attorney.

Together, limited partners and dependents are referred to as participants. Participants who are dependents, because they are still minors, can start a business when they reach 12 years of age. This allows them to save up and deposit $20,000 into the community by their 18th birthday, and possibly as early as 16.

Limited partners and their dependents reside in apartments (village buildings). Each apartment has 4 floors, with each floor containing 16 apartments. Each floor has floor has 7 – 12 limited partners, with each limited partner having 1 – 3 dependents. Each floor therefore has around 25 residents. With four residential floors, each building has approximately 100 residents. An apartment building also forms a branch.

Captains and branch presidencies

Of the approximately 100 residents in a branch, around 40 of them are limited partners.They are divided into 4 units, each of which has 10 limited partners and their dependents. The limited partner membership in a unit is diverse, containing different social groups that are reflective of the society within which a community operates.

Additionally, a unit contains members of the four main demographics: partnered males (A), partnered females (B), single females (C), and single males (D).

The 4 demographics in the branch form 4 groups, as follows:

- Group 1: partnered males and partnered females

- Group 2: single females and single males

- Group 3: partnered and single males

- Group 4: partnered and single females

Within each group, there are different subsets, known as classes, based primarily on age. There is a class for Nursery (0-2), toddlers (3 – 5), young children (6-9), pre-teens (10-12), teens (13-18), young adults (19-31), adults (32-72), and empty nesters (73+).

| Meeting week | Class 1 | Class 2 | Class 3 | Class 4 | Class 5 | Class 6 | Class 7 | Class 8 |

| Week 1 and 3 | All partnered adults | All single adults | Teen boys and girls | Pre -teens | Young children | Toddlers | Nursery | |

| Week 2 and 4 | All males | All females | Teen boys | Teen girls |

Further details on the composition of units, groups, classes, and branches, and their meeting schedules, is detailed here.

Recruitment and diversity

Captains are responsible for recruiting limited partners into the community through their council and by extension, branch. A captain does not recruit limited partners only from their demographic. Instead, they work to ensure that their recruits are diverse, considering social categorizations, gender, and social status, in addition to demographic groups.

Captains work in concert with their fellow captains in the branch presidency, and other presidencies in a village and district to ensure that the district is as diverse as possible. They are guided by present data on how diverse their district, village, and branch are, and what needs to be focused on to improve. They are also guided by community bylaws, which expressly require diversity as shown by demographic data about a population from which the community intends to recruit limited partners.

The captain serves as a service extension of the Human Relations Agency, though they also act as an interface between participants and other community agencies. For agencies that do not have operational presidencies, such agencies in the Economic and Public Administration Bureaus, captains come in handy in helping participants navigate these agencies’ automated system and other relevant tools used by the agency to deliver services.

The automated system is designed to help participants with all the help they need in matters related to various agencies, including the Human Relations Agency. However, should they run into problems, captains assist them in navigating the system, or direct them to relevant contractors who help them at a fee.

Automated system

For most of its duties, the Capital Bank works through an automated system. When a limited partner deposits their net worth in the Capital Bank, the bank issues them with a deed, which shows the money they have deposited, and the applicable terms of the legal agreement. The automated system also helps agencies as they interact with the bank.

Contractors

The Capital Bank relies on contractors to handle aspects of its operations that the automated system, agency presidency, and branch presidencies cannot handle. Contractors build the storehouse and develop the automated system. The agency also hires contractors to help in developing strategies and operational policies, and to monitor implementation as necessary.

Participants can also hire contractors to assist them in navigating the automated system. In addition, contractors working as financial professionals can help participants make better financial decisions and enable them to make the most of the community’s economic model.

Inter-agency cooperation

The 24 community agencies form three columns of 8 agencies each. There is loose collaboration between the agencies in a column. The Capital Bank Agency is part of the second column.

The Capital Bank Agency collaborates with the Utilities Agency (agency 23), which advises on the development of important utilities to secure water,electricity, among others. The bank also collaborates with the Legal Affairs Agency (agency 14) to draw up titles to issue to limited partners as they deposit their net worth, and to govern its numerous capital investment and loan agreements with agencies, districts, and villages.

Presidencies’ offices, meetings, and quarterly conferences

Offices

The Capital Bank Agency’s three agency presidencies have offices in District Building 8’s first floor, The operational agency presidency has offices on the western side. Facing them on the eastern side are the offices for trustee and regulatory agency presidencies serving the agency and District 8.

Trustees and the regulatory agency presidencies alternate their offices. Trustees have the offices in building 8 on Mondays and Wednesdays, while the operational presidencies use the offices on Tuesdays and Thursdays, as shown in this timetable:

| Building 8/ Capital Bank | Building 20/ Marketing | |

|---|---|---|

| Monday | Trustee presidency | Regulatory Bureau presidency |

| Tuesday | Regulatory Bureau presidency | Trustee presidency |

| Wednesday | Trustee presidency | Regulatory Bureau presidency |

| Thursday | Regulatory Bureau presidency | Trustee presidency |

The first floor’s layout is as follows, including other public servants who serve District 8

Working hours and meetings

Operational, trustee, and regulatory agency presidents work in their offices on a full-time basis. To allow for this, they are required to be at least 50 years of age, be experts in NewVistas concepts, and be fully retired from their business. This allows them to dedicate much of their productive time to serving the community.

On Thursday, morning, each presidency meets in the presideing president’s office. The meeting lasts for 45 minutes from 8:00 AM, with each president getting a chance to preside and another to clerrk within a month.

Every two weeks, the agency council meets. To accommodate the 12 members of the council, the presiding president’s office also takes the adjacent office to create a conference room. As with presidencies, councils order their presiding to ensure every president gets a chance to preside, and another to clerk within 6 months. The bureau council meets once a month, in the week when they do not have an agency meeting.

Quarterly conferences

Quarterly conferences are held on the last Sunday of each quarter, from 9:00 AM to 3:00 PM, with a lunch break in between. During quarterly conferences, each demographic presidency sits together in the same row.

Quarterly conferences are held in District Buildings 5 and 17. Each building has a lower and higher assembly court. The different demographic groups use the assembly courts as follows:

| Building | Assembly court | Demographic |

|---|---|---|

| 5 | Lower court | Partnered males (A) |

| 5 | Higher court | Partnered females (B) |

| 17 | Lower court | Single females (C) |

| 17 | Higher court | Single males (D) |

Branch presidencies do not attend quarterly conferences. Instead, they follow the relevant proceedings online alongside other participants.

Each of the four assembly courts has seats for 480 presidents representing the respective demographic. In the diagram below each of the 4 courts is illustrated. The ceiling of each court has an elliptical arch that enables agency presidents, who are the only ones who make a presentation during the conference, to speak with the use of a normal microphone. The 480 seats are easily rotatable to enable presidents to face whoever is speaking.

Each of the four courts has an identical arrangement and number of seats. The exact arrangement of each court can therefore be illustrated using one court, in this case, building 5’s lower court that is used by partnered males (A).

Within an assembly court, the 480 presidents are arranged in terms of demographic presidencies of 3. The Economic Bureau’s demographic presidency for partnered males (7A, 8A, and 9A) sits in the highlighted seats. Various district demographic presidencies also sit on the same row.

[1] These demographic groups are partnered males (A), partnered females (B), single females (C), and single males (D).