Agency 18 Metrics

Measurement Standards, Appraisal, and Privacy-Preserving Aggregate Representation

Agency 18 gives NewVistas a disciplined way to measure productive reality without turning measurement into bureaucracy, surveillance, finance, audit, underwriting, taxation, or operational control. This work develops Agency 18 as the constitutional measurement standards framework of the NewVistas system. Its central purpose is to make productive costs, asset burdens, overhead, lifecycle costs, appraisal assumptions, footprint categories, Community Gross Output, innovation-flow calibration, and aggregate system metrics measurable, comparable, admissible, and constitutionally usable. Agency 18 is authoritative in measurement method but strictly non-operational. It does not run businesses, finance assets, underwrite plans, audit records, hold title, administer leases, collect funds, publish as an operating agency, allocate grants, enforce payments, or control personal data. It governs the standards by which productive reality becomes visible without becoming a hidden bureaucracy or surveillance institution.

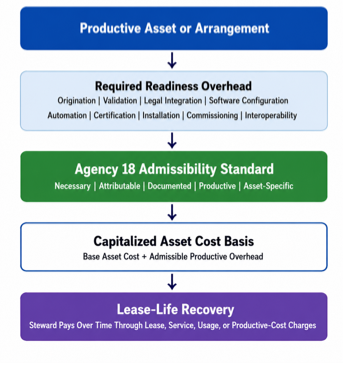

Any overhead required to originate, validate, configure, automate, integrate, certify, commission, install, legalize, or otherwise make a productive asset usable must be assigned to the cost basis of the asset or arrangement that caused it. This overhead must not be hidden as detached community expense and must not be charged upfront to the steward. Instead, the community initially pays it as part of the asset cost, the steward reviews and approves it because it affects the business plan, lease burden, DNPV appraisal, and feasibility, and the steward ultimately repays it over the productive life of the asset through lease, service, usage, or productive-cost charges. This creates a measurement system that prevents hidden subsidy, reduces wealth-based entry barriers, disciplines appraisal, preserves no-reserve doctrine, protects individual data ownership, supports innovation-flow visibility, and allows the community to understand itself statistically without becoming a public-record surveillance society.

Table 1. Agency 18

| Dimension | Agency 18 Governs | Agency 18 Does Not Do |

| Measurement | Measurement standards, admissibility rules, cost classification, metrics, appraisal representation | Does not operate businesses or productive systems |

| Capitalized Overhead | Standards for when productive overhead enters asset cost basis | Does not collect, disburse, or manage overhead payments |

| Appraisal | Disciplined present-value representation and cost-truth assumptions | Does not underwrite plans or approve business feasibility |

| Metrics | Productivity indices, cost corridors, footprint categories, QHSE thresholds, Community Gross Output | Does not create behavioral scores or individual rankings |

| Privacy | Aggregate, privacy-preserving statistical reporting | Does not own raw personal datasets or individual records |

| Innovation Flow | Measurement of approximate innovation-flow calibration | Does not allocate research grants or operate R&D |

| Constitutional Role | Make productive reality comparable and admissible | Does not become a fiscal, audit, finance, publication, or enforcement authority |

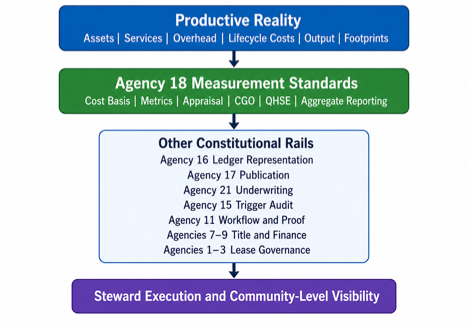

Figure 1. Agency 18 Constitutional Position

Why Agency 18 Matters

A complex productive community cannot govern itself honestly unless it can measure itself truthfully. NewVistas is a digital, service-based, lease-governed stewardship economy. The community owns the substrate, but stewards operate independent businesses through lease-based custody. This system depends on clear measurement of asset costs, readiness costs, lifecycle burdens, service costs, output, productivity, and public burdens.

If measurement is weak, overhead disappears into hidden subsidy. If measurement is too powerful, it becomes bureaucracy or surveillance. Agency 18 is designed to occupy the constitutional middle: strong enough to make productive reality visible, but too limited to operate, finance, audit, underwrite, publish, tax, or control persons.

Table 2. The Problem Agency 18 Solves

| Problem | Risk Without Agency 18 | Agency 18 Solution |

| Hidden Overhead | Setup costs disappear into general community expense | Productive overhead is attached to the asset or arrangement that caused it |

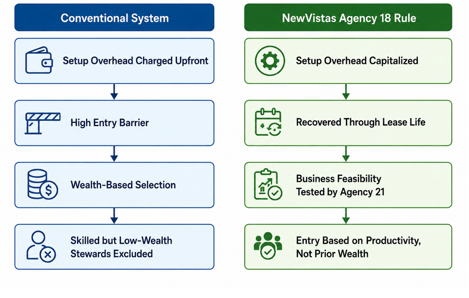

| Wealth-Based Entry | Stewards must pay setup costs upfront | Setup overhead is capitalized and recovered over asset life |

| False Feasibility | Assets appear cheaper than they really are | DNPV and lease burden include true capitalized cost |

| Over-Capitalization | Contractors or stewards may inflate configuration costs | Higher overhead raises lease burden and may fail Agency 21 underwriting |

| Reserve Drift | Lifecycle costs become idle balances or hidden funds | Lifecycle charges are contract-priced obligations, not reserves |

| Data Centralization | Metrics become surveillance | Agency 18 receives aggregate privacy-preserving outputs, not raw individual records |

| Circular Output | Internal transfers look like production | Community Gross Output counts real throughput, not synthetic churn |

| Fiscal Drift | Footprint schedules become taxes | Agency 18 measures burdens but does not collect or allocate funds |

| Innovation Funding Confusion | R&D flow becomes discretionary allocation | Agency 18 measures innovation-flow calibration but does not allocate research |

The Capitalized-Overhead Rule

Productive assets do not become usable through purchase price alone. A restaurant requires design, ventilation, safety certification, legal integration, inventory systems, workflow setup, and equipment installation. A hairdresser needs chairs, mirrors, water systems, tools, product inventory, booking systems, and space configuration. A utility steward needs telemetry, redundancy documentation, interface standards, installation protocols, and service-proof systems. A Practice Guide may need studio space, instructional tools, safety preparation, AI-supported materials, accessibility formats, and course-publication infrastructure.

If these costs are excluded from the asset basis, the measured cost is false. If they are charged upfront, skilled but low-wealth stewards are blocked from entry. Agency 18’s standard solves both problems by capitalizing admissible productive overhead into the asset cost basis and recovering it over the productive life of the asset.

Figure 2. Capitalized Overhead Without Hidden Subsidy

The methodology has five linked layers. First, Agency 18 defines how admissible productive overhead enters the capitalized cost basis of an asset. Second, the cost is recovered over the asset’s useful life through lease, service, usage, or productive-cost charges. Third, the model shows that this structure is incentive-compatible because higher overhead raises lease burden and reduces expected cash surplus. Fourth, Agency 18 disciplines DNPV appraisal by ensuring that asset value reflects real cost and enforceable productive commitments, not speculative expectations. Fifth, Agency 18 supports aggregate statistics through privacy-preserving outputs rather than raw personal datasets.

The sequence begins with the Life Plan under Agency 5 and the Business Stewardship Plan. Agency 18 does not create these plans. It governs the measurement standards that make their costs, assumptions, assets, workflows, utilities, lease burdens, QHSE requirements, and appraisal inputs legible and comparable across the constitutional system.

Table 3. Agency 18 Methodology

| Layer | What It Measures | Constitutional Purpose |

| Capitalized Cost-Basis Decomposition | Base asset cost plus admissible productive overhead | Prevents hidden subsidy and false cost representation |

| Intertemporal Lease Recovery | Recovery of cost over productive life | Removes upfront entry barriers without making overhead free |

| Incentive Compatibility | Relationship between overhead, lease burden, and cash surplus | Makes excessive overhead self-defeating |

| DNPV Representation | Present value disciplined by real cost, enforceable commitments, and lease burden | Prevents speculative feasibility and false appraisal |

| Privacy-Preserving Reporting | Aggregate statistical outputs from domain-held datasets | Allows community-level metrics without personal surveillance |

| Constitutional Chain Preservation | Separation among measurement, ledger, publication, underwriting, audit, title, finance, and lease governance | Prevents Agency 18 from becoming a hidden operating agency |

The work derives ten main results.

Result 1: Capitalized overhead prevents hidden community subsidy.

When productive overhead is excluded from the asset basis, the asset appears cheaper than it is. This creates hidden subsidy, weakens underwriting, distorts lease pricing, and hides the burden of complexity. Agency 18 eliminates this distortion by requiring admissible productive overhead to follow the productive asset or arrangement that caused it.

Result 2: Lease-life recovery removes upfront entry barriers without making overhead free.

The steward does not pay admissible productive overhead upfront. Instead, the cost is recovered over time through lease, service, usage, or productive-cost charges. Entry therefore depends on productive feasibility rather than prior wealth.

Result 3: Steward approval creates cost discipline because lease burden rises with overhead.

Although the community initially pays capitalized overhead, the steward bears the future lease burden. Higher admissible overhead increases capitalized cost, raises lease burden, and reduces expected cash surplus. This gives the steward a direct incentive to control overhead before execution.

Result 4: Over-capitalization self-terminates through Agency 21 underwriting.

Agency 18 does not reject plans as an underwriter. It measures true cost. Agency 21 determines whether the resulting lease burden is feasible. If overhead makes the plan unable to support sufficient and required obligations, the underwriting token fails.

Result 5: DNPV appraisal is overstated when capitalized overhead is excluded.

If overhead is excluded, lease burden is understated and DNPV is falsely inflated. Agency 18 prevents speculative feasibility by requiring productive overhead to enter the asset basis before appraisal.

Result 6: No-reserve discipline is preserved.

Lifecycle renewal, service correction, and compliance charges are not reserve funds. They are contract-priced obligations. Agency 18 does not collect or hold them, and stewards do not accumulate idle reserve pools.

Result 7: Agency 18 can publish macro-metrics without holding individual records.

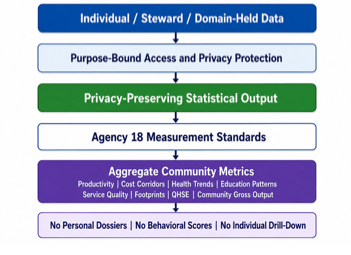

Agency 18 receives privacy-preserving statistical outputs from domain-held datasets. It may publish aggregate productivity, health, education, service-quality, footprint, and system-performance metrics, but it may not drill down into personal records.

Result 8: Community Gross Output must exclude synthetic circularity.

Community Gross Output measures real productive throughput, not circular settlement, recursive internal transfers, synthetic multiplication, or accounting churn. The goal is to know whether the community is becoming more capable, not merely more internally active.

Result 9: Footprint schedules represent burden, not Agency 18 tax authority.

Agency 18 may measure burdens related to energy, waste, emissions, material use, congestion, health burden, infrastructure strain, and innovation need. It does not collect, appropriate, allocate, or enforce payments.

Result 10: Agency 18 may measure innovation-flow calibration without becoming an allocator.

Agency 18 may define measurement standards for the approximate five percent Community Gross Output flow toward the innovation and R&D system governed elsewhere, especially Agency 13. This should be evaluated through long-duration rolling averages, not exact quarter-to-quarter equality. Agency 18 measures the ratio but does not collect funds, allocate research grants, approve research teams, or operates R&D.

Figure 3. Cost Truth and Entry Inclusion

Privacy and Digital Proof Without Surveillance

Agency 18 is especially important because NewVistas is digital-only. A digital system can easily become a surveillance system if data is centralized without limits. Agency 18 is therefore structurally barred from owning raw individual records. Personal data belongs to the individual. The community may use aggregate or statistical data, but it may not drill down into individual health, education, legal, financial, life-plan, business-plan, service, ticket, footprint, or personal history records. Doctors, mentors, teachers, hairdressers, service providers, and agencies may access personal data only when the individual provides it for a current, purpose-bound interaction. Agency 18 may measure society statistically. It may not measure persons as public records.

Figure 4. Aggregate Metrics Without Personal Surveillance

Constitutional Structure and Steward Accessibility

Agency 18 is organized through three presidencies of four: the Trustee Governing Presidency, the Regulatory Governing Presidency, and the Operational Governing Presidency. Each includes representation from four demographic divisions: partnered male, partnered female, single male, and single female. The term Operational Governing Presidency does not mean Agency 18 operates systems. It means Agency 18 must understand the practical consequences of workflows, utilization, evidence, reporting, and system outputs without administering them. District-based assisting Agency 18 presidencies give stewards local access to measurement governance. A steward dealing with productivity classification, utility reporting schema, QHSE threshold, cost corridor, appraisal assumption, digital-system output, or interoperability burden should be able to reach a constitutional office within the district order. This keeps measurements connected to productive life without creating staff bureaucracy.

Agency 18 and Domain Separation

Agency 18 is part of Bureau VI, alongside Agency 16 and Agency 17. Agency 16 governs accounting and ledger representation. Agency 17 governs publishable representation. Agency 18 governs measurable representation. These functions coordinate but must not merge. Agency 18 measures. Agency 16 records. Agency 17 publishes. Agency 21 underwrites. Agency 15 audits when triggered. Agency 11 governs systems workflow and proof. Agencies 7–9 govern title and finance. Agencies 1–3 govern lease governance. Domain agencies govern domain standards. Stewards and certified contractors execute. This separation prevents one institution from defining, measuring, publishing, underwriting, financing, auditing, and enforcing the same matter.

Table 5. Constitutional Chain of Responsibility

| Function | Assigned Rail |

| Measurement standards | Agency 18 |

| Ledger representation | Agency 16 |

| Publishable representation | Agency 17 |

| Workflow and proof | Agency 11 |

| Trigger-based audit | Agency 15 |

| Underwriting feasibility | Agency 21 |

| Title and finance | Agencies 7–9 |

| Lease governance | Agencies 1–3 |

| Research and innovation execution | Agency 13 |

| Legal form and process | Agency 14 |

| Execution | Stewards and certified contractors |

AI, Civil Law, and Boundary Protection

Agency 18 may use AI to assist classification, verification, comparison, anomaly detection, reporting consistency, translation of measurement categories, and inconsistency detection. But AI cannot become final constitutional adjudication, hidden enforcement, autonomous command, or substitute underwriting. AI-assisted measurement must remain reviewable through source traceability, version visibility, transformation intelligibility, model-use disclosure, and identifiable human responsibility.

Agency 18 also operates within external civil jurisdiction. Its internal measurement order does not nullify municipal, county, state, federal, judicial, environmental, tax, licensing, safety, or other civil-law obligations. Internal representation cannot be used to relabel or ignore external duties.

Where Agency 18 overlaps with accounting, publication, audit, systems, underwriting, legal form, or domain standards, jurisdictional questions must be resolved through constitutional process. Concerned councils of twelve should consider the matter. If unresolved, they may appoint a four-person committee with one representative from each demographic division. No final determination should be adopted unless approved by the required councils. Technical necessity, emergency convenience, software implementation, delegated workaround, nominal independence, or AI automation must not become a back door for jurisdictional expansion.

The work connects Agency 18 to several established research traditions while showing why NewVistas requires a distinct constitutional measurement framework. It draws on managerial accounting and cost capitalization to explain why costs that create future productive benefit should be assigned to the productive asset or arrangement. It uses capital budgeting to explain why costs should be recovered over time instead of hidden or charged upfront. It uses information economics to address moral hazard, adverse selection, and hidden subsidies. It uses mechanism design to show how lease burden makes overhead discipline incentive compatible. It uses institutional economics to justify separation among measurement, accounting, publication, underwriting, audit, finance, title, lease governance, and execution. It uses privacy-preserving statistics to show how aggregate metrics can be published without personal dossiers. It also connects to public finance, productivity measurement, educational metrics, health metrics, and data-governance literature. The contribution of the work is to combine these fields into a constitutional measurement architecture for a digital, service-based, lease-governed stewardship economy.

Agency 18 gives NewVistas a constitutional language for measurable reality. It makes costs visible without creating bureaucracy, enables entry without hiding subsidy, disciplines appraisal without becoming an underwriter, supports innovation without allocating funds, and produces aggregate knowledge without turning people into data profiles. Its highest contribution is disciplined visibility: the ability for a community to see itself clearly while preserving steward execution, individual data ownership, no-reserve discipline, fiduciary restraint, and constitutional domain separation.